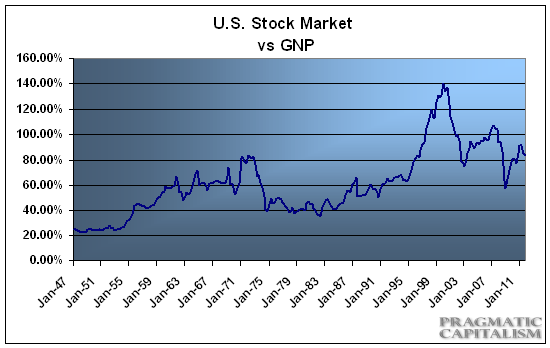

"For me, the message of that chart is this: If the percentage relationship falls to the 70% or 80% area, buying stocks is likely to work very well for you. If the ratio approaches 200%-as it did in 1999 and a part of 2000- you are playing with fire."

So stocks aren't cheap, but they're also not terribly expensive based on this measure. If the recent trend holds we could be nearing Buffett's preferred buying range in the coming years….

(click to enlarge)

Yes, its a good indicator, but a very basic indicator akin to above or below NTA. If you are buying below 100%, you are "safer", its not rocket science. This indicator ranges from 60%-140% of GNP owing to the US economic structure.

One has to bear in mind that the market cap vs GNP relationship is very different for other countries.

One of my favoured economist, Chua Hak Bin, wrote on the same topic some time back, with an Asian flavour:

Malaysian Economy More Sensitive to Crashes

The Malaysian economy is however more sensitive to crashes. The representation of households who own shares directly or indirectly is probably similar to the U.S. profile. The market capitalisation of the KLSE is however about 320 percent of GNP. This implies that a 30 percent crash in the KLSE amounts to the equivalent wipe-out of 96 percent of GNP. If the stock of wealth is about 10 times GNP, this still amounts to a dissappearance of about 10 percent of total wealth. Such a sharp fall in wealth will inevitably hurt consumer spending.

The Malaysian economy's sensitivity to stockmarket crashes has been increasing over time with the rising market capitalisation of the KLSE. During the 1987 crash, Malaysia's stockmarket capitalisation accounted for only about 90 percent of GNP. As such, the ripple effects from the 1987 crash did not have such far reaching consequences. However, with the capitalisation accounting for more than 300 percent, Wall Street's sentiment may have become inevitably linked to the Malaysian economy. This worrisome conclusion extends to Hong Kong and Singapore whose market capitalisation have both exceeded 250 percent as well.

TABLE: THE MALAYSIAN ECONOMY IS OVEREXPOSED TO A STOCKMARKET CRASH

| Countries | Market Cap/ GNP (%) | Fall in Value from 30% Crash as Percent of GNP |

| Malaysia | 320 | 96 |

| Hong Kong | 290 | 87 |

| Singapore | 250 | 75 |

| Bangkok | 109 | 33 |

| London | 105 | 30 |

| New York | 70 | 21 |

| Bombay | 38 | 11 |

| Jakarta | 35 | 10 |

Some Comforting Thoughts

There are some important factors to account for when linking market capitalisation to total wealth. First, the rather high market capitalisation of the Kuala Lumpur, Singapore and Hong Kong stockmarkets are partly a result of its openness to foreign investors. As such, a large fraction of the market capitalisation is "foreign wealth" rather than "domestic wealth." The fraction will be higher in Singapore and Hong Kong than Malaysia. If the fraction of Malaysian shares which are foreign-held account for as much as 30 percent, then the true "domestic market-capitalisation to GNP" that matters for calculating the local "wealth effect" is reduced to only 224 percent.

Second, consumption is dependent on permanent rather than current wealth. Consumers take into account their future income when deciding on their habits today. If the fall in the stockmarket is regarded as temporary rather than permanent, consumers will not treat the loss as a real loss but a temporary paper loss. As a result, consumers will not reduce their spending as sharply when faced with the fall in current wealth. A word of caution is noted however as empirical studies have provided evidence that consumption is linked to current rather than permanent wealth due to the existence of credit constraints.

My Comments: It is not the Asian markets openness that causes the 300% market cap vs GNP, or anything to do with foreign investments. Rather, its the listing mentality of the respective countries coupled with the "designed rules". In Malaysia, once you start making RM3m-5m a year, there will be predators coming to you thinking of ways to list your company.

This makes for a much lower threshold to list companies in Asia (generally) than elsewhere. Hence you may generalise that the only things not listed in Malaysia are the mamaks and mechanics (though some of the bigger mamak chains make quite decent bucket loads of money, but then they have to worry about paying real taxes if they were to list them properly).

Of course we can still use the market cap vs GNP indicator for the Malaysian market alone, maybe the range over a 20 year period could be between 200% to 400%, and you surmise that anything below 300% might be a "safer" buying territory. To me, its still more b.s. than anything.

Hence we can also surmise that a market correction of 25% in the US and a similar 25% correction in Malaysian, Singaporean and HK markets are very different. The latter 3 countries will see a more pronounced real money flow effects (shrinkage and reduced velocity of money). In most of Europe the normal indicator is around 50%, which is to say a market correction has less real impact on the real economy as a large portion of the economy there are still not listed.

That indicator is shallow and does not relate or take into account the dynamics of the markets. For example, you can tally up the holdings of indexed stocks in Malaysia held by local funds, esp local government or GLC funds. Without the exact data, I can say it has been a substantial rise over the past 10 years, in particular over the last 5 years.

What that means may be that the index could be easier to "control". This will also mean that you may be able to "engineer better" a stock market sell down, or the reverse as well. Just think how well you could "control the index" if you hold 25% of all indexed stocks, what if its 35% or 45%, maybe 65% later on.

The amount of local funds have been mushrooming and EPF has really no space to put it anymore, which is why they have to think of overseas. The other local funds have also been growing as well. Its all good and well if it does not get to the level whereby there is more "manipulative streaks" than a genuine "investing strategy for better returns". The bigger danger is that if you hold a strong hand, you could also close a stock price "artificially higher every year end" to maintain the appearance of good performance for your overall funds, even though in reality the fundamental performance of the said stock may be not exciting.

The powers to be has to be fully aware of the potential distortion this may bring and prevent this scenario from ever occurring. We are not there yet, but we need to be on guard owing to rise in investible funds in our country.

0 comments:

Post a Comment